Buying your next car? How to skip on the interest bill

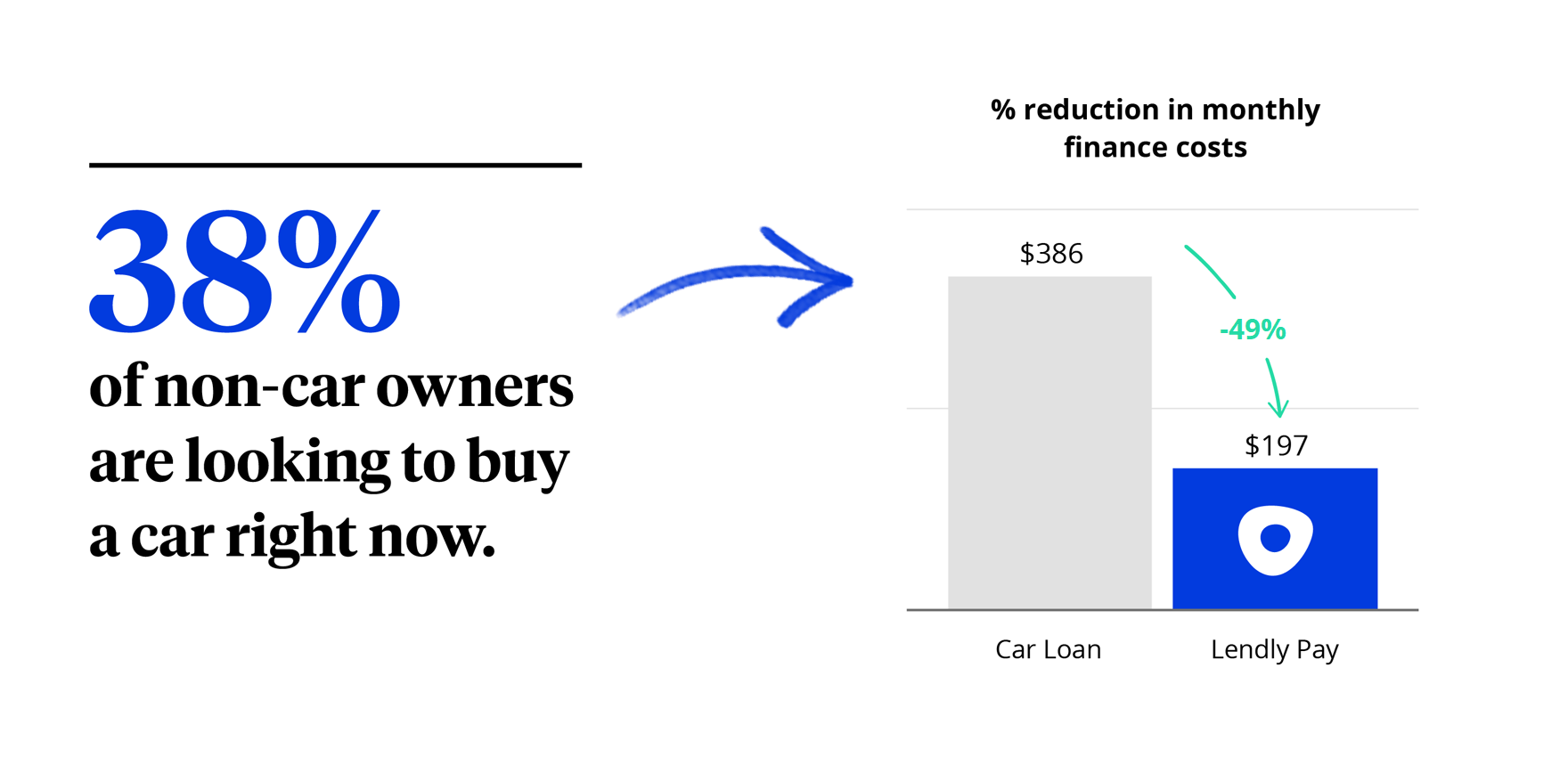

With COVID-19 changing the way people view public transportation and rideshare services, more first-time car owners are entering the market than ever before. A recent Carsales survey has shown that 38% of non-car owners are looking to buy a car right now with a remaining 58% likely to consider it.

“38% of non-car owners are looking to buy a car right now.”

But there’s a reason they haven’t owned a car previously, and usually, that has come down to cost. Regardless of the number of kilometres someone drives, there are fixed costs they’ll incur. Things like comprehensive insurance, registration and even servicing are all costs you pay even if you don’t leave the driveway, and not to mention buying the car itself.

For people that have been financially sensible enough not to own a car up until now, it’s safe to say they would want to know the cheapest way to buy one now that they’re in the market. It’s no wonder so many are finding their way to novated leasing.

A benefit that many have thought was reserved for high income, high kilometre, new car buyers; we’re here to show that every employee can save thousands via a novated lease on our Lendly Pay platform.

So if you’re not in the market for the latest and greatest European machine, and you don’t bring in a Trump size income, what does a car on a novated lease look like for you?

Case Study

Let’s look at Janet, a first-time car buyer. She makes $70,000 before tax every year, paying $15,697 in tax and taking home $4,525 every month. Janet was open to recommendations on which car would suit her best.

Step 1: Choosing the right car

Janet explained that she only was using the car to get to and from work and short trips on the weekends. She felt a small hatch would suit her best and so we suggested she should look at a pre-owned 2017 Hyundai i30 Active. That year was the start of a new model, so she gets the latest shape, still with a couple of years factory warranty remaining, modern safety and heaps of tech (even Apple CarPlay), 12-month service intervals and low-cost tyres all for a $15,000 purchase price.

Step 2: Calculate a budget for running costs

Janet drives just 10,000 kms each year and felt a 3-year term would suit her needs best. To help her calculate a monthly budget we first had to figure out the total bill to run a Hyundai i30 for 30,000 kms over 36 months.

- Fuel: $3,785

- Comprehensive insurance: $4,020

- Registration: $2,610

- Maintenance: $2,244

- Tyres: $770

- Roadside assistance: $257

- Total running costs: $13,686

Having calculated the total costs over 36 months, Janet agreed to set a monthly budget of $380 to pay her car bills.

Step 3: Calculate the tax savings

Then to access tax benefits on a car that’s used 100% for personal use, the tax office says Janet needs to buy her car using a novated lease. When we put it on a three-year lease the monthly repayment looked like this:

- Finance cost: $386

- Less tax savings: $189

- Net lease cost: $197

Janet was going to spend $380 each month just to run her car, no matter how she chose to pay for the vehicle itself. However, by putting it on a novated lease, she didn’t put any money in upfront and her net finance costs were reduced from $386 to $197 a month.

Which means she will only pay a total of $7,100 in net finance costs over the 3 years. Then at the end, Janet will only owe $7,000 on the car. If she wants to pay the car out and keep it, she would have only paid a total of $14,100 for a car with an original purchase price of $15,000.

For Janet to find a cheaper way to own a car, she would have to find a bank that not only didn’t charge fees or interest but also gave her $900 to take the loan out. In addition to all that she has the added comfort that if she is made involuntarily unemployed during the lease, she has lease protection insurance that will make her repayments and provide reimbursement for running costs while she is looking for work.

Lendly Pay at your work

It’s easy to see why people who want to make the smartest financial decision when it comes to buying and running a car, use Lendly Pay.

If you’re one of the 86% of non-car owners who are actively looking or starting to think about buying a car, we’re here to help. If you already own a car and you’re not using Lendly Pay, it’s not too late to get started.

Ready to start saving? Find out how much you could save with Lendly Pay.